I Cut My Home Insurance Bill From $6,500 to $3,800 By Doing One Thing. Here Is What That Tells You About Florida Right Now.

Jul 13, 2026

I Cut My Home Insurance Bill From $6,500 to $3,800 By Doing One Thing. Here Is What That Tells You About Florida Right Now.

By Jeff Levine, Broker Associate at Lux Places Group, RE/MAX Services, and 2026 Vice President of Florida Realtors

My home is 30 years old.

It does not have a brand new roof. It does not have impact windows on every opening. It does not sit on the highest elevation in Boca Raton. By every Florida insurance underwriting standard I have lived through for the last decade, my house should still be one of the expensive ones to insure.

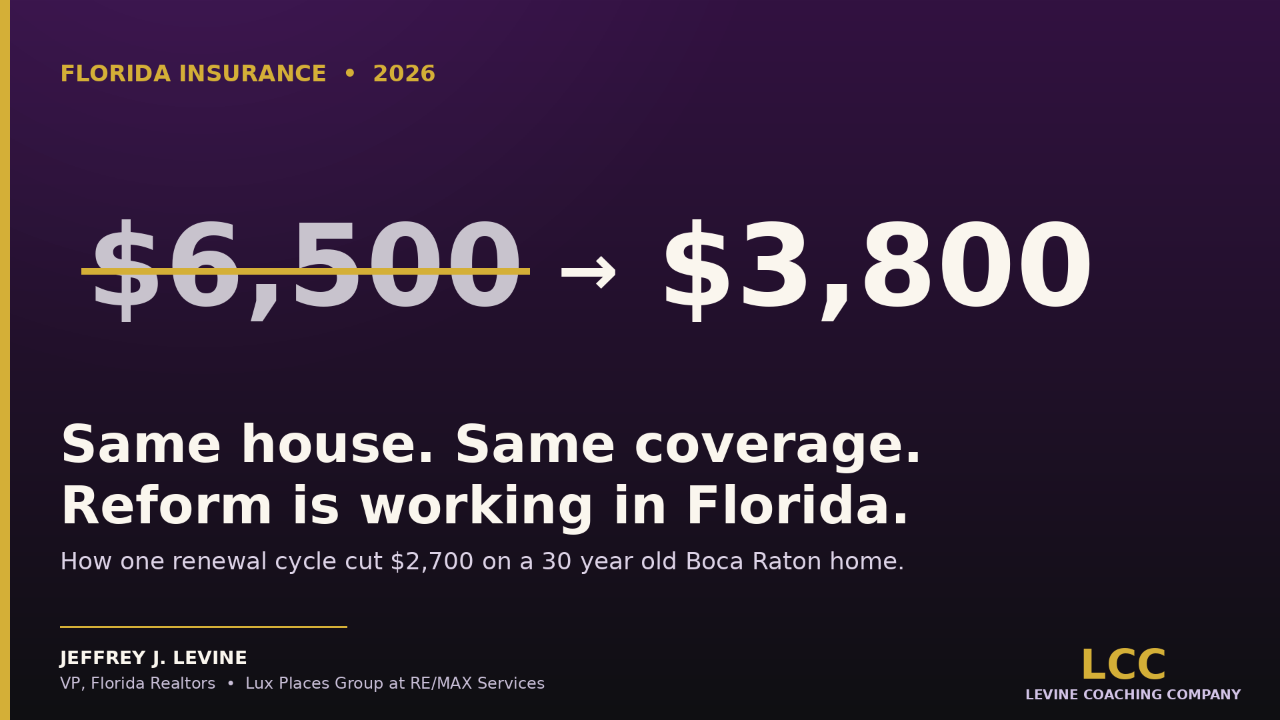

Last year, my homeowners premium was $6,500.

This year, after one renewal cycle and a few hours on the phone, my premium is $3,800.

That is a $2,700 drop on the same house, the same roof, the same address, and the same family. Same coverage limits. Same deductibles. I did not raise my wind deductible. I did not strip down my replacement cost coverage. I did not switch to some thinly capitalized carrier that nobody has heard of.

I shopped my policy.

That is the entire story.

And the only reason that story is even possible in Florida in 2026 is because the insurance market here looks completely different than it did three years ago. That part is not a coincidence. That part is policy, advocacy, and years of work by the people who refused to accept that Florida homeowners were stuck.

What Actually Happened in My Renewal

When my carrier sent over the renewal at $6,500, my first instinct, like most homeowners, was to grind my teeth, write the check, and move on. That is what almost everybody does. It is also exactly the reason the old market got away with what it got away with for so long.

Instead, I called an independent insurance agent and asked the question I should have been asking every single year. What else is out there for my house?

She came back with three competitive quotes within 48 hours. Three. Not one. Not two. Three carriers, all licensed in Florida, all financially rated, all willing to write my 30 year old home in Palm Beach County.

The lowest of the three came in at $3,800.

I called my existing carrier to give them the chance to match. They could not. Or would not. Either way, the answer was the same. I moved the policy. The new policy bound the same week.

Why This Was Not Possible Two Years Ago

If I had tried this exercise in 2023, my agent would have laughed. There were not three carriers willing to write my house. There were not even three carriers actively writing new business in many Florida ZIP codes. Most of the market had either pulled out, gone insolvent, or stopped taking new policies entirely.

Today, Florida has 30+ active carriers in 2026 and the cheapest one changes year to year. Since the enactment of these reforms, 17 new insurance companies have entered Florida, increasing competition. Dozens of homeowners and auto insurers have filed for rate decreases.

That is not a small number. That is a market structurally healing in real time.

And it is showing up at the kitchen table.

What the Data Says About the Broader Market

I am not the only homeowner with this story.

Under the approved rate filings, the vast majority of Citizens policyholders statewide will receive lower premiums, with a statewide average reduction of 8.7%. More than 330,000 policyholders across all 67 counties will see decreases.

The numbers are even more aggressive in South Florida, which historically carried the highest premiums in the state. In South Florida, policies covering owner-occupied single family homes would see the largest average rate decreases: 14.1% in Broward and Miami-Dade and 11.9% in Palm Beach.

For Citizens Property Insurance specifically, the state's insurer of last resort, this is historic. Citizens Property Insurance's Board of Governors approved 2026 rate recommendations on December 10 that would reduce average rates for policyholders for the first time since 2015.

The first time since 2015. Take a moment with that.

And the trend extends well beyond Citizens. The practical effect for 2026: rate increases that averaged 30 to 45% in 2022 to 2024 have flattened to single-digit increases (or in some inland markets, flat to slightly down renewals) for properly inspected homes with newer roofs.

How the Market Got Here

You cannot understand my $2,700 savings without understanding what changed underneath it. This part matters, because what I want every Florida homeowner reading this to do is shop their policy this year. But what I want every Florida Realtor, every advocacy supporter, and every member of our state association to understand is what made that shopping worthwhile.

For years, Florida was the litigation capital of the homeowners insurance world. Just prior to the passage of these reforms, 76 percent of the country's homeowners insurance lawsuits originated in Florida, home to just 9 percent of U.S. homeowners.

Read that twice. Nine percent of the homeowners, 76 percent of the lawsuits.

That math is not normal. It is not a coincidence. And it is what drove carrier after carrier out of the state, which is what drove the cost of what remained through the roof.

The Legislature acted. SB 76 (2021) changed litigation rules surrounding disputed insurance claims. SB 2A (2022) limited the assignment of attorney fees to third parties (assignment of benefits, or AOB), and disincentivized frivolous claims. HB 837 followed in 2023, reshaping the broader tort framework.

These were not popular bills with every interest group. They were hard fights. And they have, by every objective measurement, started to work.

Frivolous lawsuits against property insurance companies dropped 25% in the first half of 2025 as compared to the same period in 2024, and the number of filings to initiate litigation was approximately 4,000 in November 2024, down from 8,000 per month in early 2023.

Cut the lawsuits in half, and the carriers come back. The carriers come back, and competition returns. Competition returns, and a 30 year old house in Boca Raton goes from $6,500 to $3,800.

Florida Realtors Was in This Conversation From Day One

I want to be specific about something, because the people who showed up in Tallahassee for these reforms deserve to be named.

Florida Realtors, representing more than 230,000 members across this state, was an active participant in the property insurance reform conversation from the beginning. Our association did not sit on the sidelines while the market collapsed. Our members felt the affordability crisis at the closing table every single day. We could not write contracts, we could not close deals, and we watched buyers walk away when the insurance number came in.

The association made the case at every level. Members called legislators. Volunteer leaders testified. Government affairs staff stayed in the room for every draft. The position was consistent and the position was right: a functional insurance market is not a luxury. It is the foundation of homeownership in Florida.

A new analysis published in February 2026 by the Perryman Group, covered by Florida Realtors, makes the economic case even clearer. Legislative tort reforms passed in 2022 and 2023 prevented Florida property and casualty insurance premiums from rising an average of 14.5% and spurred economic growth across the state. Avoiding those higher costs preserved an estimated $4.2 billion in additional business activity and more than 29,000 jobs.

$4.2 billion. 29,000 jobs. That is what advocacy looks like when it actually moves policy.

As the 2026 Vice President of Florida Realtors, I will tell you that the work is not finished. There are still affordability pressures. There are still ZIP codes and home profiles where the market is tight. And there will be efforts every legislative session to roll back the reforms that made the current recovery possible. The advocacy continues, because the market is not yet where it needs to be for every Floridian.

But where it is today, compared to where it was 24 months ago, is night and day. And my renewal is one data point in a story that thousands of Florida homeowners are now living.

What This Means For You Right Now

If you are a Florida homeowner reading this, here is what I want you to do before your next renewal.

One. Call an independent insurance agent who can shop multiple carriers. Not your existing carrier's customer service line. Not a captive agent who can only quote one company. An independent agent with access to a panel of carriers writing new business in Florida.

Two. Get a current wind mitigation inspection. The fastest wins are a fresh wind mitigation inspection (often unlocks 15 to 30% in credits), bundling home and auto (10 to 25% discount), raising your AOP deductible to $2,500, and re-shopping annually. If your last inspection is more than five years old, you are almost certainly leaving money on the table.

Three. Treat your homeowners policy the way you would treat any other major recurring expense. Shop it. Compare it. Negotiate it. The days of 'I have always been with this carrier' being a smart strategy are over. Loyalty is not rewarded in the current Florida market. Inertia is punished.

Four. If you are buying, selling, or even just considering a move in Florida, build insurance into the conversation early. A good Realtor will help you understand the insurance picture for any specific property before you make an offer. That conversation belongs at the front of the process, not the night before closing.

The Bigger Picture

I started this post talking about $2,700. That is real money to my family, and it is real money to every Florida homeowner who is going to have the same conversation at their next renewal this year.

But the bigger picture is this. Markets respond to policy. Policy responds to advocacy. And advocacy responds to organized, consistent, principled voices showing up in the rooms where decisions get made.

Florida's insurance market collapsed because the rules created an unsustainable environment. It is recovering because the rules changed. And the rules changed because a lot of people, including the 230,000 members of Florida Realtors, kept showing up and making the case.

The next time someone tells you that advocacy does not matter, or that one association cannot move a market, you can point them to my renewal letter.

A 30 year old house. Same coverage. $6,500 last year. $3,800 this year. That is what changed.

Jeff Levine is Broker Associate and Team Leader of Lux Places Group at RE/MAX Services in Boca Raton, Florida, and founder and CEO of Levine Coaching Company. He serves as the 2026 Vice President of Florida Realtors, representing more than 230,000 members statewide. With nearly 30 years of real estate experience and oversight of more than 10,000 transactions, Jeff coaches and trains real estate professionals and association leaders on building businesses, teams, and organizations that scale with clarity.